Backdoor Roth IRA Tax Calculator

Backdoor Roth IRA Calculator

Calculate your tax impact from a backdoor Roth IRA conversion based on your IRA balances and tax situation. Avoid the pro-rata rule trap and maximize your tax-free retirement savings.

If you make over $200,000 a year and want to save for retirement with tax-free growth, you’ve probably hit a wall. The IRS doesn’t let high earners contribute directly to a Roth IRA. But there’s a legal, widely used workaround called the backdoor Roth IRA. It’s not a loophole-it’s a strategy built into the tax code. And in 2025, with legislative threats looming, it’s more important than ever to understand how it works, when to use it, and how to avoid costly mistakes.

Why High Earners Need the Backdoor Roth IRA

In 2025, if you’re single and earn more than $161,000, or married filing jointly and earn more than $240,000, you can’t contribute directly to a Roth IRA. That’s not a typo. Even if you’re making $400,000, have a solid emergency fund, and are maxing out your 401(k), you’re locked out of the best retirement account for tax-free withdrawals.

That’s where the backdoor Roth IRA comes in. It lets you bypass the income limit by going around it, not breaking it. You contribute after-tax money to a traditional IRA-no deduction-and then quickly convert it to a Roth IRA. The IRS allows this because it never banned Roth conversions, only direct Roth contributions. This trick has been around since 2010, and despite repeated attempts in Congress to shut it down, it’s still legal as of November 2025.

Why bother? Because Roth IRAs grow tax-free. No taxes on dividends, no taxes on capital gains, and no taxes when you withdraw in retirement. If you’re in a high tax bracket now and expect to be in one later, this is one of the few ways to lock in today’s rates and avoid future taxes on your retirement savings.

How the Backdoor Roth IRA Works: Step by Step

Doing this right takes precision. Mess up one step, and you could owe thousands in unexpected taxes. Here’s how it’s done in 2025:

- Open a traditional IRA if you don’t already have one. You can do this with any brokerage-Vanguard, Fidelity, Charles Schwab. It doesn’t matter which.

- Contribute $7,000 (or $8,000 if you’re 50 or older). This is the 2025 limit for non-deductible contributions. You’re not taking a tax deduction, so the money goes in after-tax.

- Convert immediately. Within days, transfer the full amount to a Roth IRA. Don’t wait. Even a 1% gain on $7,000 means $70 in taxable income. The goal is zero growth between contribution and conversion.

- File IRS Form 8606. This is non-negotiable. You must file it for both the year you contribute and the year you convert. The IRS audits backdoor Roth filers more often than most people realize-93% of 2024 audits on this issue were because Form 8606 was missing or wrong.

That’s it. Simple in theory. But here’s where most people fail: the pro-rata rule.

The Pro-Rata Rule: The Silent Killer of Backdoor Roths

This is the #1 reason people get burned. The IRS doesn’t look at your Roth conversion in isolation. It looks at all your traditional IRAs, SEP IRAs, and SIMPLE IRAs-across every bank or brokerage you own.

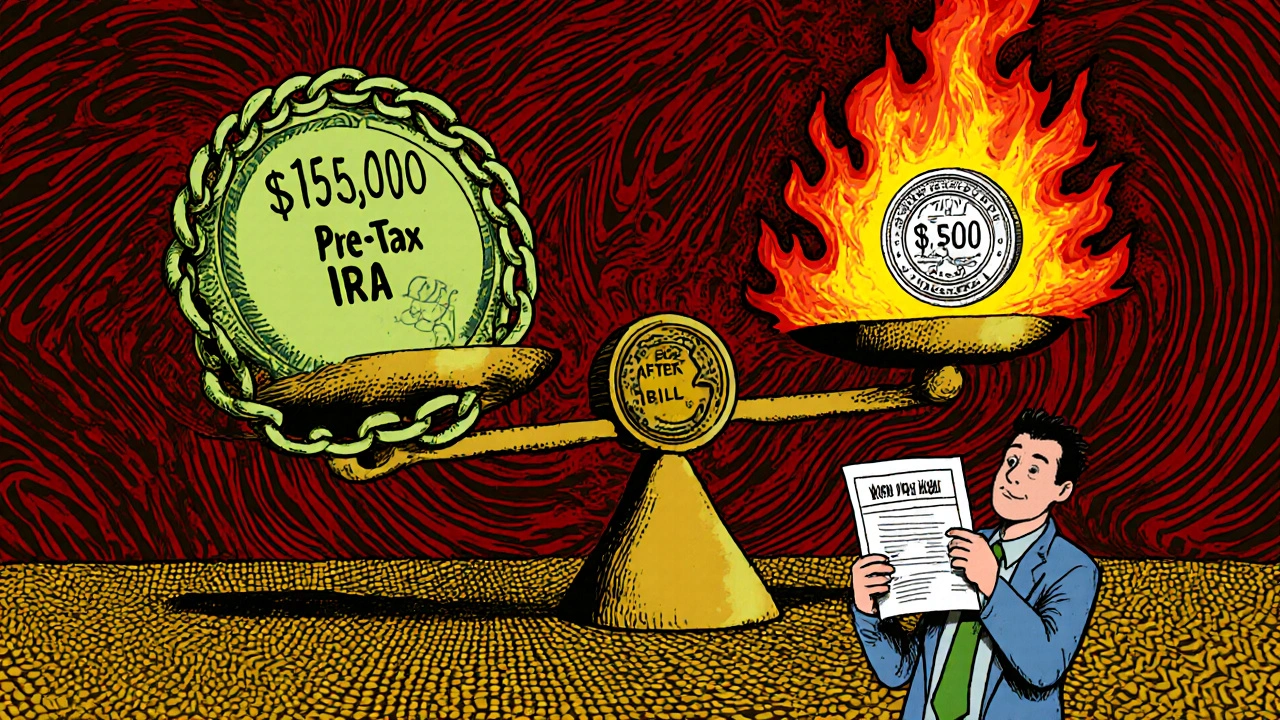

Let’s say you have a $150,000 traditional IRA from a past 401(k) rollover. You open a new traditional IRA and put in $7,000 after-tax. You convert that $7,000 to Roth. Sounds clean, right?

Wrong. The IRS says: you have $157,000 total in IRAs. $150,000 is pre-tax. $7,000 is after-tax. That’s 95.5% pre-tax, 4.5% after-tax. So when you convert $7,000, $6,685 of it is taxable. You pay taxes on nearly all of it-even though you only put in $7,000 after-tax.

That’s not a mistake. That’s how the rule works. And it’s not just your own IRAs. If your spouse has pre-tax IRAs, those count too. And if you have a SEP IRA from side work? That counts too. The IRS aggregates them all.

Real-world example: A 48-year-old doctor in Arizona had $93,000 in pre-tax IRAs. He did a $7,000 backdoor Roth. He expected $0 tax. He got a $6,510 tax bill. That’s 93% of his conversion being taxed because of the pro-rata rule.

How to Fix the Pro-Rata Problem

You can’t ignore it. But you can neutralize it. Here’s how:

- Roll pre-tax IRAs into your 401(k). If your employer plan allows it (62% of major employers do in 2025), move your old traditional IRAs into your 401(k) before December 31 of the year you plan to do the backdoor Roth. Now your IRA balance is $0. You contribute $7,000. You convert $7,000. No pro-rata. Clean conversion.

- Don’t have a 401(k)? Consider a solo 401(k) if you have side income. You can roll IRAs into it. Or wait until you change jobs and roll into your new employer’s plan.

- Wait until you’re retired. If you’re close to retirement, you can roll your pre-tax IRAs into a 401(k) after you leave your job. Then do the backdoor Roth in the year you’re unemployed or have low income.

Don’t try to do the backdoor Roth if you have pre-tax IRAs unless you’ve cleared them first. Otherwise, you’re not saving on taxes-you’re just creating a bigger tax bill later.

The Mega-Backdoor Roth: Bigger Contributions, Same Rules

If you’re making $300,000+ and your employer offers a 401(k) with after-tax contributions, you can do something even bigger: the mega-backdoor Roth.

In 2025, you can contribute up to $69,000 total to your 401(k)-$23,000 in pre-tax or Roth elective deferrals, and up to $46,000 in after-tax contributions (if your plan allows it). Only 37% of 401(k) plans offered this in Q2 2025, but it’s growing.

Here’s how it works: you contribute $46,000 after-tax to your 401(k). Then, you convert that $46,000 to a Roth 401(k) or roll it into a Roth IRA. The conversion is tax-free because you already paid taxes on the money.

This isn’t for everyone. You need:

- An employer plan that allows after-tax contributions

- An employer plan that allows in-plan Roth conversions or in-service rollovers

- Enough income to max out the $69,000 limit

But if you qualify? You can add $46,000 a year to your tax-free retirement bucket. That’s $1.38 million over 30 years, tax-free. No other retirement account comes close.

Alternatives to the Backdoor Roth

What if you can’t do the backdoor Roth? You have other options:

- Traditional IRA: If your income is below $77,000 (single) or $123,000 (married), you can deduct your contribution. But you pay taxes on withdrawals. Not ideal if you’re in a high bracket now.

- Health Savings Account (HSA): Triple tax advantage-deductible contributions, tax-free growth, tax-free withdrawals for medical expenses. 2025 limits: $4,150 individual, $8,300 family. Only if you have a high-deductible health plan.

- Roth 401(k): No income limits. You can contribute up to $23,000 directly. If your employer matches, you get free money too. But you’re capped at $23,000-not $7,000 or $46,000.

None of these match the backdoor Roth’s combination of unlimited income eligibility, $7,000 annual contribution, and tax-free growth. That’s why it’s so popular.

Who Should Avoid the Backdoor Roth?

It’s not for everyone. Here’s when you should skip it:

- You have large pre-tax IRAs and can’t roll them into a 401(k)

- You’re planning to retire in the next 5 years and need the money soon

- You’re in a very low tax bracket now and expect to be in a higher one in retirement (rare for high earners)

- You’re not organized enough to file Form 8606 every year

Also, don’t do it if you’re already doing a mega-backdoor Roth. You don’t need both. Focus on the bigger pot first.

Legislative Risk: Is the Backdoor Roth Going Away?

Here’s the scary part: Congress has tried to kill this strategy five times since 2010. In July 2025, the House Ways and Means Committee approved language to ban after-tax IRA conversions to Roth IRAs. The Senate will vote before December 2025.

If it passes, the change would likely take effect in 2026. That means if you want to do a backdoor Roth, you have to do it before January 1, 2026.

That’s why Charles Schwab reported a 43% spike in backdoor Roth conversions in Q3 2025. People are rushing. Vanguard processed 1.2 million backdoor Roth conversions in the first half of 2025-up 27% from 2024.

But here’s the good news: even if it’s banned, the mega-backdoor Roth through 401(k)s is still safe. And Roth 401(k)s aren’t going anywhere. The real threat is to the $7,000 annual Roth IRA contribution path.

Real Stories: Successes and Disasters

On Reddit, user ‘TaxSmartMD’-a physician earning $450,000-rolled his $180,000 pre-tax IRA into his hospital’s 401(k) in 2023. Since then, he’s done a $7,000 backdoor Roth every year. Five years later, he’s added $35,000 in tax-free contributions. No tax bill. No issues.

Another user, ‘IRA_Oops’, didn’t roll anything. He had $150,000 in pre-tax IRAs. He did a $7,000 backdoor Roth in 2024. His tax bill? $12,300. He thought he was saving money. He lost $5,300.

On Bogleheads.org, 78% of people who cleared their pre-tax IRAs first succeeded. Only 32% succeeded if they didn’t.

The pattern is clear: do it right, and you win. Do it wrong, and you pay.

Final Checklist for 2025

Before you start, run through this:

- Do you have any pre-tax IRAs, SEP IRAs, or SIMPLE IRAs? If yes, roll them into your 401(k) before December 31.

- Do you have a traditional IRA with $0 balance? If not, open one.

- Can you contribute $7,000 (or $8,000) after-tax? Yes? Good.

- Will you convert within 3-5 business days? Yes? Good.

- Will you file Form 8606 for both contribution and conversion? Yes? Good.

- Are you doing this before January 1, 2026? Yes? Then you’re safe-for now.

If you check all these boxes, you’ve done it right. No guesswork. No surprises. Just tax-free growth waiting for you in retirement.

Can I do a backdoor Roth IRA if I have a 401(k)?

Yes, having a 401(k) doesn’t stop you. In fact, it helps. You can roll any pre-tax IRAs into your 401(k) to avoid the pro-rata rule. Just make sure your plan allows rollovers from IRAs. Most large employers do.

Do I pay taxes when I convert my traditional IRA to Roth?

Only on the pre-tax portion. If your traditional IRA has $0 pre-tax money (because you rolled it out), then your conversion is 100% tax-free. If you still have pre-tax money in any IRA, you’ll owe taxes on the percentage that’s pre-tax. That’s the pro-rata rule.

What happens if I forget to file Form 8606?

You could get audited. The IRS uses Form 8606 to track after-tax contributions. Without it, they assume all your IRA money is pre-tax. That means they’ll tax your entire conversion-even the part you already paid taxes on. Penalties can include interest and fines. File it every year, even if you think you don’t need to.

Can my spouse and I both do backdoor Roths?

Yes. Each person can do their own backdoor Roth, up to the annual limit. But the pro-rata rule applies to each person individually. If your spouse has pre-tax IRAs, those count for their conversion, not yours. You each need to manage your own IRA balances.

Is the backdoor Roth IRA safe from IRS audits?

It’s not immune, but it’s not a red flag if done correctly. The IRS knows the strategy is legal. What triggers audits is missing Form 8606, incorrect calculations, or not rolling out pre-tax IRAs. If you follow the steps, file the form, and keep records, you’re fine. 93% of audits are due to paperwork errors, not the strategy itself.

What if the backdoor Roth is banned in 2026?

If it’s banned, you won’t be able to do new backdoor Roths after December 31, 2025. But any Roth IRAs you already have stay open. You can still contribute to them in future years if you qualify under new rules. The mega-backdoor Roth through 401(k)s is likely to remain available. Consider accelerating your conversions in 2025 if you’re eligible.

Comments

The pro-rata rule is such a sneaky bastard, isn't it? I spent three months digging through IRS publications before I realized my $120k rollover IRA was silently torpedoing my backdoor Roth. It's not about the mechanics-it's about systemic tax architecture designed to punish the financially literate who don't have corporate 401(k) access. The fact that the IRS aggregates all your IRAs like some kind of financial panopticon is almost Marxist in its efficiency. And yet, here we are, gaming the system with 401(k) rollovers like financial ninjas. If this gets banned in 2026, we're not losing a loophole-we're losing the last vestige of individual tax sovereignty for high earners. Welcome to the new Gilded Age, where your retirement strategy depends on your employer's plan design.

Ugh. Another ‘tax hack’ post from someone who thinks ‘after-tax’ means ‘free money.’ You’re not a financial wizard-you’re a tax accountant’s dream client. The mega-backdoor Roth? Please. Only people with $300k+ incomes and employer plans that actually work (looking at you, Google and Apple) can even play this game. Meanwhile, the rest of us are over here contributing to Roth IRAs with $500 a month and praying the IRS doesn’t notice we’re still alive. You’re not building wealth-you’re just optimizing for a tax code written by and for the 0.1%. And don’t even get me started on Form 8606. I’ve seen people cry over that thing. It’s not finance. It’s bureaucratic performance art.

Thank you for laying this out so clearly. I’ve been hesitant to attempt the backdoor Roth because I didn’t fully grasp the pro-rata rule-and now I see how easily it could backfire. I had a small traditional IRA from a past job and assumed it was irrelevant. Turns out, it wasn’t just relevant-it was a ticking time bomb. I rolled it into my 401(k) last week, and I’m planning my $7,000 contribution this month. The fact that you included real examples-like the doctor who got hit with a $6,500 tax bill-made it click in a way no textbook ever did. I’m also relieved to hear the mega-backdoor is still safe. That’s going to be my next project once I clear this first step. You’ve saved me a lot of stress.

I did backdoor Roth last year. Form 8606 filed. No tax bill. 😊